Where Craft Meets Innovation

Helping founders and innovators grow their spirits brands, from the first pour to full-scale production and distribution.

How Minimum Order Quantities Quietly Kill Cash Flow in the Alcoholic Beverage Industry

For many new beverage brands, the logic feels straightforward.

Start with the smallest possible production run. Limit inventory exposure. Conserve cash until demand is proven.

On paper, this approach appears disciplined. In practice, it often creates the exact conditions that make profitability harder to reach.

Minimum order quantities are not inherently the problem. Suppliers implement them for practical reasons. Equipment needs to be set up. Production lines need to run efficiently. Freight becomes more economical at scale. These constraints exist because the system is optimized for throughput, not for early-stage brands testing demand.

The real issue emerges when lower upfront spend is mistaken for lower long-term cash burn.

At small production volumes, the economics of beverage alcohol can deteriorate quickly. Distributor and retailer margins remain relatively fixed, which means any inefficiency at the production level is absorbed by the brand.

A brand may be able to place a small order of a few hundred units. Nothing strictly forces a larger run. The constraint is not feasibility, but the way costs increase and margins compress at low volume.

At lower volumes, setup costs for labels, cans, and packaging are distributed across fewer units. Freight shifts from full truckload shipping to palletized Less-Than-Truckload (LTL) shipments, which can cost two to three times more per pallet and introduce additional handling points where damage can occur. Quality control also becomes more expensive, since the same number of defects represents a larger percentage of the run.

These factors combine to increase the cost per unit in ways that are not always obvious at first glance.

This is where contribution margin becomes critical.

In simple terms, contribution margin is the profit remaining after production costs are deducted from revenue. It is what the brand uses to cover fixed expenses such as salaries, rent, software, marketing, and sales efforts.

At small production volumes, that margin often compresses before it is fully understood. The product may still appear viable on the shelf. Consumers may still purchase it. Retailers and distributors continue to earn their margins. But the economics shift upstream, and the brand absorbs the inefficiency, sometimes to the point of losing money on each unit sold.

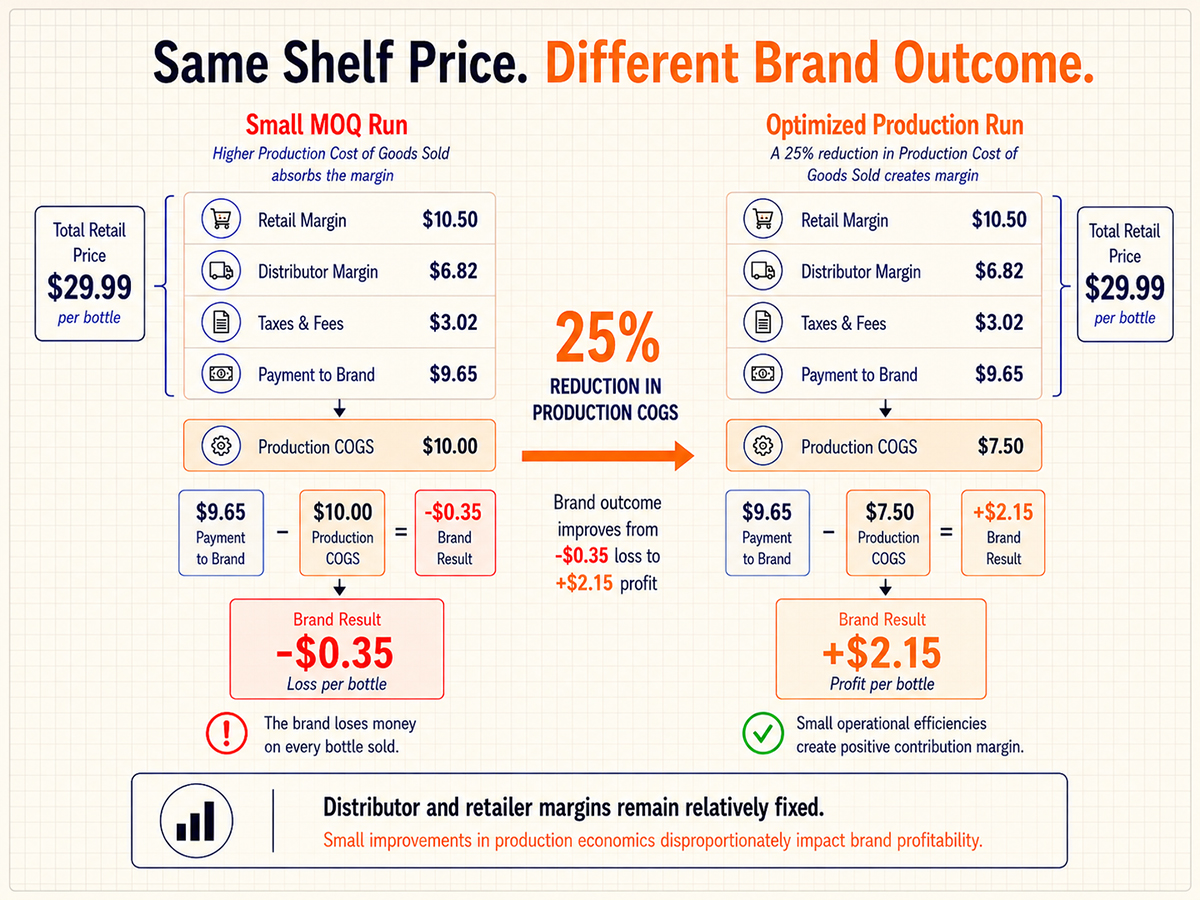

This dynamic becomes much clearer when the pricing structure is modeled directly.

Consider two bottles sold at the same $29.99 retail price. One is produced at a smaller scale with higher per-unit costs. The other comes from a slightly larger run that reduces total COGS by roughly 25 percent.

The retail price remains the same.

Distributor margins remain unchanged.

Retailer margins remain unchanged.

What changes is the outcome for the brand.

In the smaller run scenario, the brand loses money on each bottle sold. In the larger run, the same product becomes profitable.

The difference is not necessarily driven by cheaper materials or lower quality. It often comes from straightforward operational improvements. Shipping six pallets instead of moving a single pallet through LTL freight can materially reduce cost per unit. Setup costs are distributed across a larger number of bottles. Packaging and labor become more efficient. Small savings across multiple cost categories accumulate into a meaningful shift in margin.

To the consumer, both bottles look identical. Underneath, the economics are completely different.

Lower margins do not just reduce profitability. They change how the entire business behaves.

New beverage brands already face high costs to enter the market. Customer acquisition is expensive. Distributors and sales teams require incentives to prioritize an unproven product. Retailers often expect promotions, bill-backs, or introductory support.

At the same time, fixed costs continue regardless of sales volume. Salaries, rent, compliance, and software expenses do not decrease simply because production volume is low.

If the profit remaining after production costs is too small, each additional sale contributes very little toward covering those fixed expenses. In some cases, it may not cover them at all.

This creates a situation where growth requires additional capital rather than generating it.

That is the contradiction behind very small production runs. They reduce the initial cash outlay, but can extend the time required to reach profitability, increasing the total amount of capital the business consumes along the way.

This does not mean that the risk of excess inventory should be ignored.

Holding excess inventory ties up capital, increases storage costs, and introduces the possibility of expiration, particularly for products like RTDs and canned cocktails.

But underproduction introduces a different type of risk, especially in beverage alcohol where distribution relationships and shelf space are constantly in flux.

Consumers rarely wait for out-of-stock products to return. The first purchase is a trial. The second purchase determines whether the brand retains that customer. If the product is unavailable at that moment, the customer often switches to a competing option.

Retailers respond similarly. Products that cannot maintain inventory are replaced.

Distributors are even more pragmatic. They manage portfolios, not individual brands. If a product repeatedly struggles to maintain inventory, distributors may shift focus toward another supplier that can keep product moving consistently. Re-entering that slot later is often significantly more expensive than maintaining it in the first place.

Operationally, correcting an out-of-stock situation usually requires rush production, expedited freight, and reactive decision-making that further erodes margin.

Inventory can certainly trap capital. But insufficient inventory can damage momentum at the exact moment a brand is trying to establish velocity.

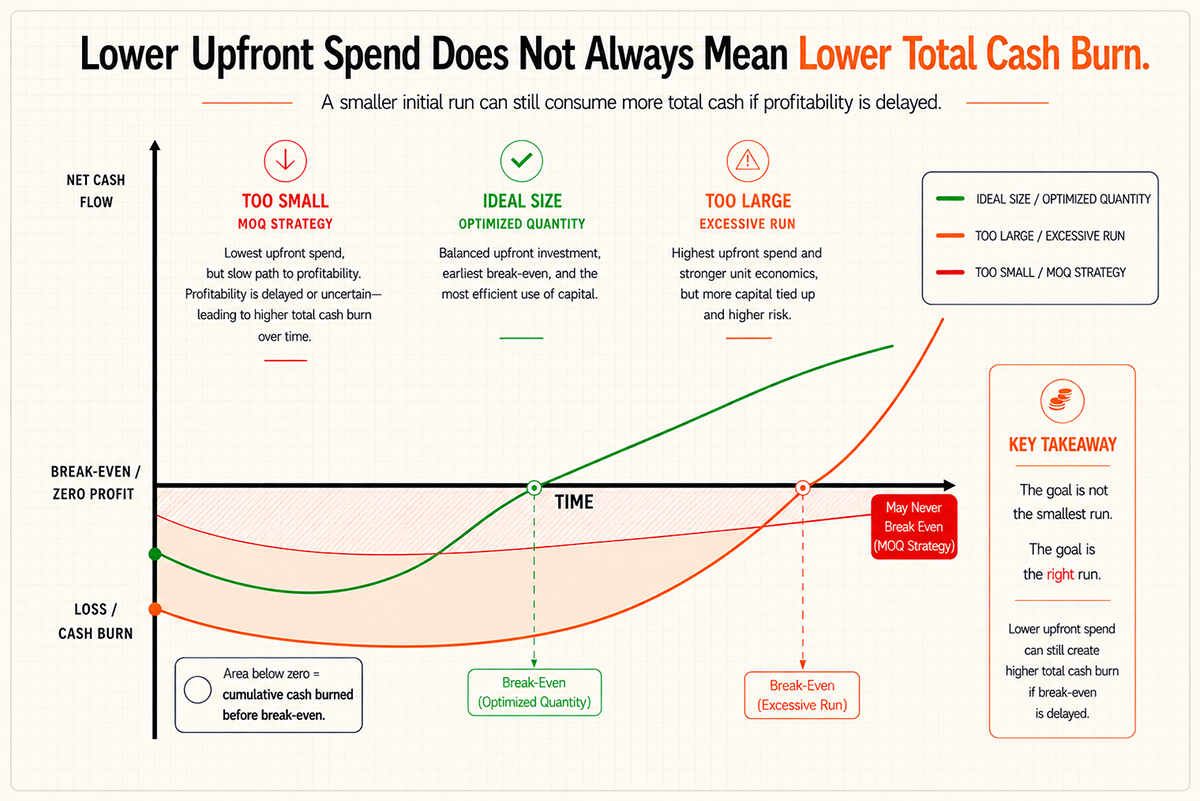

The goal is not simply to minimize production spend. It’s to reach a sustainable margin before fixed operating costs consume too much capital.

This is where financial modeling becomes useful.

When different production scenarios are modeled, a pattern tends to emerge. Very small runs reduce upfront cost but often lead to weaker margins and a longer path to profitability. Very large runs improve unit economics but can tie up significant capital in inventory.

Between those two extremes sits a more sustainable operating range.

A production level where:

contribution margin becomes healthy

freight efficiency improves

setup costs become diluted

inventory remains manageable

sales velocity can realistically support the run

Visually, this often resembles an “area under the curve” problem. The longer a company operates below profitability, the larger the cumulative cash burn becomes. Faster progression toward sustainable margin can actually reduce total capital consumption over time, even when the initial production spend is higher.

That dynamic is not always intuitive. But it becomes much clearer once the economics are modeled directly.

For this reason, production planning in beverage alcohol is becoming more analytical and model-driven.

Brands are increasingly evaluating:

landed cost under different freight scenarios

contribution margin at different production volumes

inventory exposure relative to sales velocity

time-to-profitability across multiple run sizes

how operating costs stack up against real sales performance

The goal is not to eliminate uncertainty, which is not possible in a consumer market, but to make tradeoffs visible before capital is committed.

This is where advanced production methods and modeling tools are beginning to play a larger role. More flexible production approaches and better forecasting allow brands to evaluate multiple scenarios and choose a path that aligns with both demand and financial constraints.

BarrelRM helps producers see the full picture before production begins. By modeling MOQ constraints, inventory exposure, and time to revenue, brands can make decisions based on cash flow, not just supplier minimums. The result is tighter runs, faster capital recovery, and fewer surprises sitting in storage.

If you’re planning a launch or rethinking your next production cycle, let’s start the conversation.

Get in Touch